Ben Lorica and Evangelos Simoudis on Humanoids, Software-Defined Vehicles, and Global Export Controls.

Subscribe: Apple • Spotify • Overcast • Pocket Casts • AntennaPod • Podcast Addict • Amazon • RSS.

In this episode, Ben Lorica and Evangelos Simoudis of Synapse Partners to break down the most significant developments from CES 2026. They explore the explosion of humanoid robotics and the transition toward software-defined vehicles before diving into a deep analysis of the shifting US-China export controls on AI chips. The conversation highlights the growing importance of open-weights models and the geopolitical complexities of maintaining semiconductor leadership in an increasingly fragmented global market.

Interview highlights – key sections from the video version:

Related content:

- Rodney Brooks: Predictions Scorecard, 2026 January 01

- Books by Evangelos Simoudis:

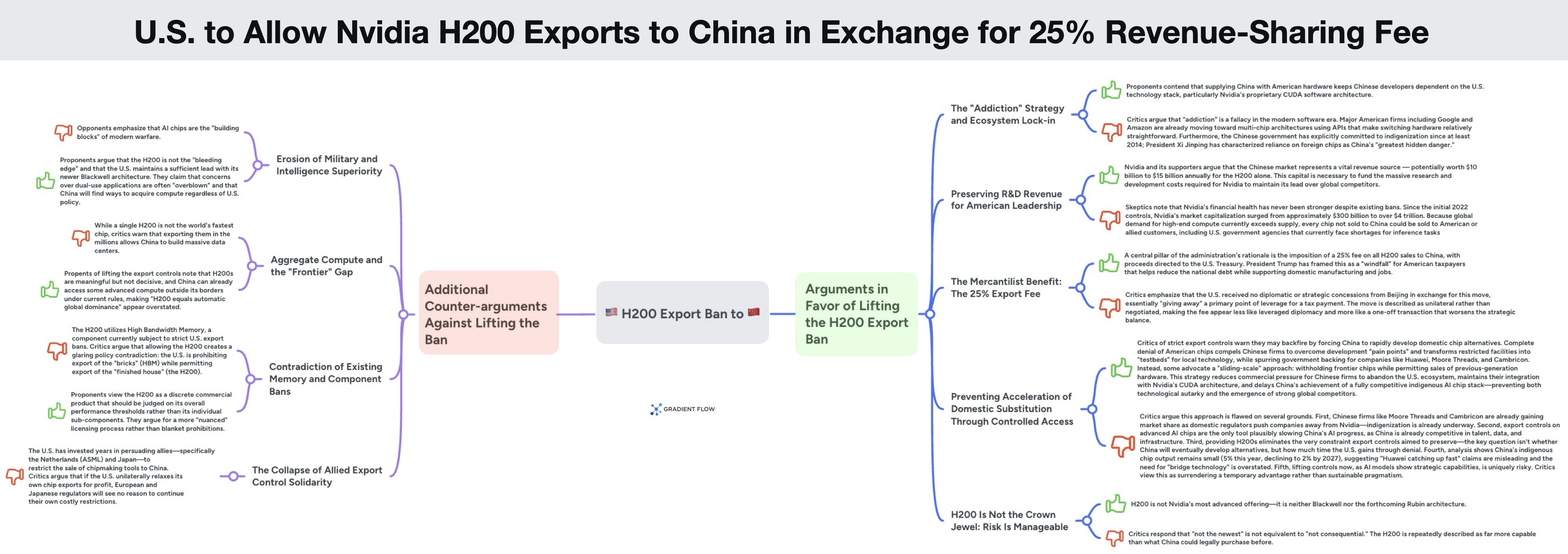

- Graphic: The case for and against the H-200 Exports Controls

- Ben Lorica and Evangelos Simoudis → Is AI a Utility? Defining Usability and Public Trust

- Ben Lorica and Evangelos Simoudis → How AI Is Reshaping Jobs, Budgets, and Data Centers

- Ben Lorica and Evangelos Simoudis → Stop Piloting, Start Shipping: A Playbook for Measurable AI

- Ben Lorica and Evangelos Simoudis → When AI Eats the Bottom Rung of the Career Ladder

- Ben Lorica and Evangelos Simoudis → Why China’s Engineering Culture Gives Them an AI Advantage

- Ben Lorica and Evangelos Simoudis → Beyond the Agent Hype

{kind=link}

Support our work by subscribing to our newsletter📩

Transcript

Below is a polished and edited transcript.

Ben Lorica: All right, we’re back for our first conversation with Evangelos Simoudis of Synapse Partners. His blog is at corporateinnovation.co. We’re recording this on the morning of January 9, 2026. The references we’ll be citing can be found in the episode notes on thedataexchange.media. If you’re watching this on YouTube, please hit the subscribe button; if you’re listening to this on a podcast, subscribe wherever you get your podcasts.

Topic number one: Evangelos and I have been following the Consumer Electronics Show (CES), the big conference in Las Vegas this week. We want to cover some of the key takeaways. Evangelos, what is your first key observation?

Evangelos Simoudis: It was a humanoids conference. To put some meat on the bones, there were humanoids everywhere. Over 30 companies were exhibiting humanoids—most of them Chinese, a few Korean, and even fewer US-based.

A couple of things stood out to me. First, there were a lot of demos, but many were tele-operated. I still didn’t see many that I could envision functioning in a real-world environment. I also think we are over-emphasizing humanoids compared to the broader category of adaptive robots.

Another thing that surprised me was what I call “the magnificence of the hand.” Many of these robots have several degrees of freedom—the largest was probably about 20—but they are still unable to get the hand to operate in every environment because of the complex sensors we have in human hands. That points to the work that still needs to be done.

Furthermore, while they are called autonomous, they weren’t; as I mentioned, they were tele-operated and had minders nearby. I haven’t seen many real applications yet. I’ve written a paper about applications in the automotive industry and assembly lines, but I’m not certain how close we are to that. There are implications for what still needs to be done to the robot, but we also need to think carefully about what it means for the human on the assembly line.

I’ll end this remark by noting that Hyundai said they are going to start manufacturing up to 30,000 such robots over the next couple of years. They exhibited the Atlas robot, which has been in development for many years and is now a collaboration with Google. They plan to introduce it in the factory they are building in Georgia. This is an interesting development because if the administration expects these new automotive investments to be a source of large employment opportunities, the introduction of this type of robotics may actually curtail those employment numbers.

Ben Lorica: A couple of quick observations. One, as I mentioned before we started recording, Rodney Brooks just released a massive essay with a large section on robotics. He lists ten observations about humanoid robots. For those who don’t know, Rodney Brooks is an elder statesman of robotics and is still very active with a new startup. He has some key observations that we will link to.

My other question for you, Evangelos, is about the number of companies you saw. I assume many are venture-funded. What are the investors thinking? Do they expect a return on these investments?

Evangelos Simoudis: I’m not certain if all of them are venture-funded. For example, Hyundai’s work is not. However, during 2025, we saw a significant influx of venture capital into companies like Figure, Apptronik, and 1X, as well as several European companies.

Ben Lorica: And specifically, are they investing in humanoid robots?

Evangelos Simoudis: Yes, the names I mentioned are all developers of humanoid robots of different form factors.

Ben Lorica: So, if you’re an investor, what is the rationale?

Evangelos Simoudis: I believe many are thinking of it as a “shiny object”—something that captures the imagination. Elon Musk’s claims about turning Tesla into an adaptive robotics company with Optimus has attracted a lot of attention and followers.

I don’t believe many investors have thought through the broad implications and applications. We talk about manufacturing and logistics, and investor presentations often mention Amazon’s robotics in distribution centers, but a broad set of applications hasn’t been fully explored.

Finally, I recently heard an interview with the CEO of 1X, which makes a more consumer-oriented humanoid. He admitted that most activities today require a tele-operator and that the range of tasks their robots can perform is still very narrow. We have a long way to go. I encourage listeners to skim Rodney Brooks’ post because he has nearly 50 years of experience in this field and makes excellent points that are worthwhile for investors and entrepreneurs to understand.

Ben Lorica: What is your second observation?

Evangelos Simoudis: The second takeaway relates to software-defined vehicles (SDVs) and AI. I’ve written extensively about this; my last book, The Flagship Experience, was all about SDVs and AI.

First, the influence of the Chinese market is being felt, and companies are now openly talking about bringing SDVs to market.

Ben Lorica: You might want to give a one-sentence definition of software-defined vehicles for our listeners.

Evangelos Simoudis: A software-defined vehicle is one where the hardware and the software are cleanly separated, and much of the vehicle’s functionality is defined by software. Tesla is the prototypical example, and Rivian is another.

We are seeing an increasing number of SDVs entering the market; even some GM vehicles can now be considered software-defined. More importantly, to have a true SDV, we need to move toward “zonal architectures.” At CES this year, companies like BMW and Rivian spoke openly about transitioning from the first iteration of these architectures (which were domain-based) to zonal ones. The biggest advantages of zonal architecture are fewer hardware components with more computing power and the ability to update a larger percentage of the vehicle over the air (OTA). In advanced zonal architectures, upwards of 80% of the vehicle can be updated OTA.

The second point is AI in the cabin. Previously, we focused on AI for autonomy, but now we’re seeing it used for the occupant experience. Mercedes announced a collaboration with Google and Microsoft to work on agents for cabin interaction. BMW announced a relationship with Alexa Plus. Hyundai and others made similar announcements.

Ben Lorica: What about Apple? Was Apple a presence in this category?

Evangelos Simoudis: No, Apple never comes to CES. Apple’s play will likely be around CarPlay, but in the announcements automakers made regarding AI in the cabin, there was no mention of Apple. Almost everyone offers CarPlay, but not from the perspective of integrated AI.

The last point regarding autonomy is that I saw it broken into two parts. There was a shift in emphasis toward personal autonomous vehicles rather than just robotaxis. There was a lot of discussion on how to offer Level 4 autonomous vehicles for personal use.

Much of this is motivated by Tesla’s goals. However, the biggest announcement came from Nvidia, which deepened its relationship with Mercedes. Ford also announced they would have a Level 3 autonomous vehicle by 2028 for a relatively low price—around $30,000.

One last thing: 30 automakers and tier-one suppliers announced a consortium to develop open-source software for software-defined vehicles. If they can pull it off, it would be a very good thing for the industry.

Ben Lorica: How about one last takeaway from CES?

Evangelos Simoudis: This one is a bit self-serving. In my second book, Transportation Transformation, I discussed various models for robotaxis. At the conference, Zoox, Uber, and Waymo were all present. We are seeing different models emerge: Waymo has the full stack, from technology to service; Uber is partnering with Waymo but also developing its own vehicles through partnerships with Nuro and Lucid. It was rewarding to see these models, which I wrote about in 2020, come to fruition six years later.

Ben Lorica: One observation I had is that the major chip providers were also at CES. Nvidia announced the Rubin platform, AMD had announcements regarding Ryzen and ROCm, and Intel and Qualcomm were there as well.

Evangelos Simoudis: As vehicles become more intelligent, both in the cabin and for autonomous operation, more computing power is necessary. If we want to offer intelligence in the cabin, we need to focus on Edge AI. This requires specific chips that operate within the vehicle with specific power and inference characteristics. Qualcomm’s partnership with BMW is just as important as Nvidia’s partnership with Mercedes.

Ben Lorica: We should devote a segment to the state of autonomous vehicles next month, as that requires a longer discussion.

Our second topic is export controls, specifically regarding Nvidia’s H200 line of chips. In early December, the Trump administration announced a relaxation of the previous policy held under the Biden administration.

The interesting thing is that while I was putting together a graphic summarizing the arguments for and against these controls, I couldn’t find an official written policy document. Usually, the White House releases a document, but every article about this refers back to a Truth Social post. As best as we can tell, export controls will be relaxed, and the US government will take a cut of the revenue from those exports.

Since then, Chinese authorities have told local companies to stop ordering these chips, encouraging them to purchase domestic AI chips instead. There is confusion about how impactful the US policy will be if the Chinese government dissuades its own companies from importing them.

The proponents for lifting export controls often cite the “addiction” argument: if you prevent Chinese companies from using US chips, they will develop domestic alternatives, which hurts US companies in the long run. However, that argument feels less compelling now. Even in the West, there has been a psychological breakthrough; Google announced Gemini 3 was trained completely on TPUs, Cerebras has viable chips for inference, and AMD is investing heavily in its ROCm software stack.

Another argument is that if you give China controlled access to US chips, their local industry will progress more slowly because they won’t need to innovate. But as I said, the Chinese government is already seeding that domestic flywheel. Finally, Nvidia argues they need the revenue from China to fund their R&D to preserve US leadership. But as critics point out, Western companies and the US government can’t get enough Nvidia chips as it is—there is plenty of revenue available without China.

Evangelos Simoudis: You laid that out very nicely. China has stated through Xi Jinping that they want to be technologically self-sufficient. Whether we give them access to Nvidia chips or not, China is determined to develop its own semiconductor industry. The West’s actions—including those of the Dutch company ASML—are slowing them down, but China is determined to develop advanced capabilities by hook or by crook.

Furthermore, those of us at the forefront of AI are realizing you can do a lot with Small Language Models (SLMs). It is often more important to develop vertical models of a reasonable size than to rely solely on massive foundation models.

We are also seeing that we can optimize existing models to run on existing semiconductor technology. We don’t always need the latest GPU to achieve our goals because we understand better how these models work and how they can be fine-tuned.

One last point: I am intrigued by the “open weights” strategy China has adopted. If these models work well and don’t require the most advanced computing power, companies like Nvidia will face headwinds. If an enterprise develops a prototype using an open-source Chinese model on-premise, it’s unlikely they will switch to a different model when they go to production.

Ben Lorica: To close, I’ll cite the arguments from those who support strict export controls. First, if the US acts unilaterally without coordinating with allies like the Netherlands or Japan, it weakens the overall strategy. Second, softening controls without getting anything in return gives up a major point of leverage. Third, we don’t yet know the full military applications of frontier models. Finally, there is still a true hardware advantage; Huawei’s own roadmap projects their share of chips in this area will actually decline by 2027. The US should exploit that advantage while it lasts.

This is a complicated issue, and we probably should have a more formal policy than a social media post.

Evangelos Simoudis: The two sides are feeling each other out while technology advances very quickly on both sides.

Ben Lorica: I agree. The Chinese have rushed to fill the gap in the open-weights ecosystem. While US labs release open-weights models, it is clearly a secondary priority for them compared to the Allen Institute in Seattle, which released a truly open-source model with data and code. The West will need to step up there.

Thank you, Evangelos.

Evangelos Simoudis: Thank you, Ben.